Beer Marketer's Insights

A late Oct raid by federal agents punctuated growing scrutiny of one of the largest and most consequential US alc bev bizzes, piquing interest and plucking at broader sense of uncertainty or even unease. TTB and IRS agents "descended on" the Union City, CA location of Southern Glazer's Wine & Spirits (see last issue). Meanwhile, SGWS is currently defending against 2 private antitrust lawsuits in federal ct, one filed by ecommerce startup Provi (see Apr 22 issue), the other by a group of small indie retailers in CA.

In no other sizable state has beer world flipped more over the years than in California. AB used to be half the mkt, now Constellation is #1. And the #1 distrib, Reyes Beer Division, sells more than half the beer in the state, buying most of that in just the last 5 yrs. Pace of change started to pick up speed in 2008, after formation of ABI and MC. Kicked into higher gear after Constellation forced consolidation from many AB distribs, moving that volume to Reyes Beer Division.

Following 1st half in which depletions down 3%, Molson Coors' US biz much improved in Q3, with sales-to-retailers down 0.9%. Marks MC's best quarterly performance "in over a decade," co noted. Tho still down slightly, MC depletions continued on better trajectory: declined 4.3% in Q1, -1.7% in Q2, down 0.9% last qtr. Shipments also steadied, +1.4% in Q3 after more than 5% drop in first half, we estimate (see above). Still lagging STRs following 2+ pt gap thru FY 2021. And up against 3% shipments gainin Q4 2021, after soft comps in Q3 (-5%). Net sales in Americas climbed 6.8% in Q3 with sales per hectoliter +7.5%. But global pre-tax income dropped $207 mil, 43% to $273 mil, largely driven by inflation.

Shipments Slipped ~2.5% Thru Sep; $$ +4% in Oct IRI; Most Top Co Volume Still Soft Except STZ

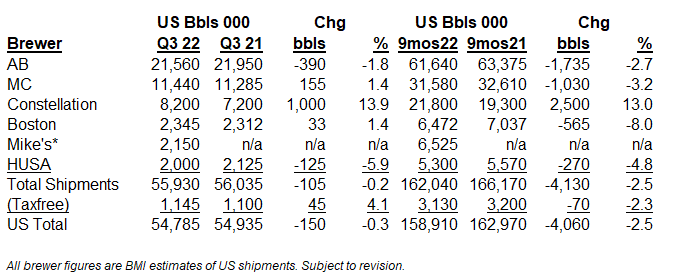

US beer shipments improved in Q3 against easy comps, tho still slipped 2.5% and shed over 4 mil bbls for 9 mos thru Sep 2022, INSIGHTS estimates. Anecdotally, a tuff start to Q4 on volume too. But huge 8% increase to avg price/case put $$ sales up 4% for 4 wks thru Oct 30 in IRI multi-outlet + convenience data, even as volume slipped 4%. In fact, beer $$ growth rate outpaced both spirits (+3.9%) and wine (-2.1%) in Oct scans, including 2X faster growth rate vs spirits in the latest 2 wks thru Oct 30. So beer gained significant share of total alc bev $$ for period. When was last time that happened? Industry shipments vs revs likely to be two very different stories in 2022.

MI Closer to Permanent Drinks-to-Go; Voted Down with Other Measures in CO, Despite $26-Mil Spend

State senate in Michigan overwhelmingly supported bill to permanently allow cocktails-to-go from on-premise licensees, DISCUS announced today. Vote was a runaway, 37-1, sending bill to state House. If House agrees and Governor Whitmer signs, MI would join 18 other states plus DC in extending the pandemic-era change in perpetuity. The state's current law extends the practice thru end of 2025. Eleven other states have temporarily extended on-premise drinks-to-go. As with other key issue for DISCUS, RTDs, advocacy lifts up voices of small craft distillers. "Cocktails to-go were instrumental in helping many Michigan distilleries navigate and survive the challenges of COVID," prexy of state craft distiller org and owner of Long Road Distillers, Jon O'Connor commented.

Avg case of a price of beer almost $30 for last 4 weeks thru Oct 30 in IRI multi-outlet + convenience data. That's quite a bit higher than in recent past and tho volume trends ain't great (-3.6%), only slightly worse than 12-week trend, -3.1%. And significantly better than YTD trend: down 4.8%. What's more, total beer $$ sales up 4% for 4 weeks, compared to just flat YTD. So far at least, second beer industry price increase of yr seemingly having little ill effect nationally.

Definitely more deal activity than usual in 2d half of 2022. INSIGHTS tracked 14 distrib deals since Sep 1, including these 2 recently announced to employees. Burkhardt Sales & Service will sell its 4.2-mil-case distribs in St Augustine and Gainesville to Mitchell Companies of Mississippi, which owns AB distribs Mitchell Distributing in MS and Chesapeake Bev in MD. Mitchell Companies will sell about 22 mil cases after this deal is done early next yr.

Craft Holds In Latest Scans, But Not Craft Prices; Founders Falls Off for 4 Wks; Case Gain/Loss Game

Steady low single-digit growth continues for craft in IRI off-premise scan data thru Nov 3. But some interesting watchouts worth highlighting as the segment finds its way thru dynamic moment in US beer biz. Craft $$ up 2.5% for 4 wks and now up 2.9% yr-to-date in IRI multi-outlet + convenience. Notably, craft cases up even stronger, +2.8% for 4 wks. So average craft case-prices just slightly soft, down 11 cents to $38.05. Craft pricing still solid YTD, up almost 1% to $37.85. And as has become standard in craft, looks like pricing impacted more by shift to larger pack sizes, especially in cans, than discounting.

NBB Reactions and Read-Thrus: Local Backlash, ESOP Questions, Coors Connections, Deals Beget Deals

Just like the US craft segment as a whole, reactions to craft M&A have matured. And fragmented. Responses to the New Belgium deal on social media are perhaps even more varied than responses we’ve seen in the past, the vitriol somehow more poisonous, the congratulations more hearty. Direct responses from consumers to NBB’s tweet announcing the acquisition seem overwhelmingly negative. Many industry observers and insiders shared a decidedly more positive outlook. But plenty of others took a ‘wait-and-see’ approach, perhaps reflecting a recognition that no one deal is precisely like another.

Correction/Clarification; To ESOP or Not to ESOP? When reacting to the deal online, many folks drew attention to the company’s Employee Stock Ownership Plan and the fact that those employees still need to approve the deal. At its two breweries and in other parts of the country, New Belgium employs about 700 folks total. As we wrote yesterday, over 300 of them will get $100K in retirement funds due to the deal. Many other NBB employees did not yet enjoy the benefits of employee ownership, however.

Note tho that our use of past-tense “sold” in first line of yesterday’s article not quite right: NBB and Lion signed agreement but deal not yet closed. Also, total Lion has 4,000 employees, not Lion Little World Bevs, which has 200-300 employees, Lion spokesperson explained.

When asked (admittedly by her own request) if she would follow the same path and initiate an ESOP if she had to do it over again, NBB founder Kim Jordan concluded that “the jury is out on that question,” during talk at Calif Craft Beer Summit in Long Beach this fall. “I honestly have mixed feelings,” she said at the early Sep event. Lion/Kirin had already entered the picture, as local press revealed this week. Discussions about this deal were ongoing, tho Kim said nothing about them publicly. She did acknowledge that an ESOP is “capital intensive,” creating “a lot of mouths to feed.” So tho an ESOP works for the craft beer biz “on the philosophical side,” the financial realities are much more complicated. In the end, the $190-mil payout to current and former employee owners is likely to represent about half of estimated purchase price for New Belgium, as we suggested yesterday.

Coloradoan: “Akin to...Kraft”; Kirin’s $2.8-Bil War Chest; “Decision-Making” Outside Ft Collins Local press in Colorado may have hit the hardest against announcement. The deal “is akin to selling to Kraft Foods or Nestle,” NBB’s hometown paper The Coloradoan wrote, covering the deal again this morning after initial coverage yesterday. “Kirin is also part of the Mitsubishi Financial Group, a massive holding company similar to 3G Capital or Berkshire Hathaway,” the paper summarized thoughts of asst professor of supply chain mgmt at local Colo State Univ, Zac Rogers. “They have their fingers in a lot of different pies,” Zac said.

But Kirin obviously looking to push its fingers much deeper into global craft pie, too. It purported to have a $2.8-bil budget for global acquisitions, likely to be focused on US and European craft deals, its CEO Yoshinori Isozaki said in Feb of this yr, according to Fortune. That’s a larger number than CBN had heard and represents quite a war-chest capable of pulling together quite an array of craft assets. This is “a major step in its global craft brewing ambitions,” The Australian explained before summing up previous Lion Little World Bevs deals, starting with top Aussie craft Little Creatures in 2012.

Tho the Coloradoan’s coverage began with that somewhat damning assessment of the deal, a separate columnist explored the ways NBB is “inseparable” from Fort Collins. Column provides glowing details of the co’s long history of charitable donations and giving back to its community, totaling many millions of dollars. “I sure hope” those connections continue, the columnist concludes, offering a toast to NBB, its employees and its deep connections to the city. But hard to hide that NBB’s future now tied to decisions made far away from Northern Colorado. The tie up with Kirin does open up possibility of broader intl distribution of NBB beer, as CSU asst prof Zac Rogers pointed out, but “now the decision-making power is somewhere else,” he summed up.

Denver Post: Combined with Coors Departure, a “Major Blow” to Colo Beer Perhaps even more dour stance taken by Denver Post, clearly reflecting on the deal’s announcement in such close proximity to Molson Coors’ decision to close its Colorado offices and move its HQ to Chicago. NBB deal is “another major blow to the Colorado beer industry in the last two months,” the paper kicked off its coverage. And it’s no surprise. This is a city and a state that just learned how beer M&A transforms a company over the long-term. This fall’s decision by Molson Coors occurred 14 years after Coors and Molson first merged, 11 years after that company’s JV with SABMiller to form MillerCoors in the US and 4 years after Molson Coors got sole ownership of that US entity as part of AB InBev’s sell-off of some of SABMiller’s assets.

The Coors “move means Colorado has lost one of its most iconic, long-running brands ― and with it, a big part of the state’s corporate identity,” the Post contended. Undoubtedly, many Coloradoans have long derived a sense of pride from their state’s leadership in beer, whether culturally or economically. Those folks can be forgiven for seeing NBB’s choice thru the lens of Molson Coors’ recent choice and therefore fearing not what will happen with New Belgium in the immediate future, but what could happen over many years.

San Francisco: Magnolia to Be Fully Owned by Lion Little World Bevs Too Before the deal closes, New Belgium will need to do another deal, acquiring the rest of San Francisco’s Magnolia Brewing, a spokesperson confirmed with SFGate. Recall, NBB came together with Belgian brewery Oud Beersel and Dick Cantwell to acquire Magnolia as part of that co’s bankruptcy filing. So Magnolia will also become part of the Lion Little World Bevs US craft arsenal, giving it a second foot-hold in the lucrative (yet expensive) San Francisco market, where co already has a sizeable brewpub for its Little Creatures brand.

So Magnolia’s story also follows a familiar pathway: a large build-out requiring lots of debt leading directly to one deal and now another. Recall, Kim connected the deal directly to a pair of prior choices requiring a ton of capital and therefore debt: the co’s ESOP and its Asheville, NC brewery. “Any craft brewer who expanded capacity and/or took private equity money in the past decade, expecting double-digit growth to continue unabated, is facing some seriously unpleasant realities,” founder of Brooklyn Brewery Steve Hindy shared with CBN. Again, one deal often leads to another.

Latest on Dogfish/Boston distrib network consolidation, craft and "4th category" oppys, new media campaigns and more were fleshed out during wide-ranging panel discussion with Boston Beer founder/chairman Jim Koch and Dogfish Head founder Sam Calagione at our annual Beer Insights Seminar in NYC earlier this week.